Intel Reports Q1 2023 Earnings: A Record Losing Quarter Goes Better Than Expected

by Ryan Smith on April 28, 2023 11:45 AM EST- Posted in

- CPUs

- Intel

- Financial Results

Kicking off our coverage of the first earnings season of the year for the tech industry, we as always start with Intel. The blue-hued blue-chip is the first out of the gate to report their results for the first quarter of 2023, with Intel picking up the pieces after a rough end to 2023, and a rather painful start to 2023. With revenue down on a yearly basis almost across the entire board thanks to a major, industry wide slump in client and server sales, Intel’s focus has been on battening down the hatches to weather this rough period, while preparing for an eventual (if modest) upturn in the market later this year.

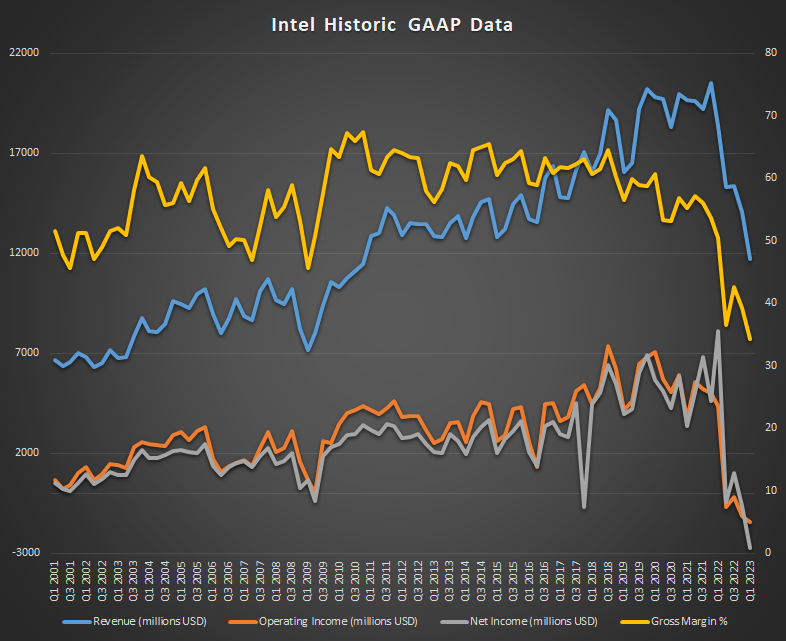

For the first quarter of 2023, Intel booked $11.7B in revenue, a precipitous 36% drop from the year-ago quarter. As was the case in Q4, Intel is in the midst of a major industry slump, which has hit revenues hard and operating/net incomes even harder. Intel closed the quarter in the red on an operating income basis, losing $1.5B, and the company’s overall net loss was a staggering $2.8B on a GAAP basis.

| Intel Q1 2023 Financial Results (GAAP) | ||||||

| Q1'2023 | Q4'2022 | Q1'2022 | Y/Y | |||

| Revenue | $11.7B | $14.0B | $18.4B | -36% | ||

| Operating Income | -$1.5B | -$1.1B | $4.3B | -134% | ||

| Net Income | -$2.8B | -$661M | $8.1B | -134% | ||

| Gross Margin | 34.2% | 39.2% | 50.4% | -16.2 ppt | ||

| Client Computing Group | $5.8B | $6.6B | $9.3B | -38% | ||

| Datacenter and AI Group | $3.7B | $4.3B | $6.0B | -39% | ||

| Network and Edge Group | $1.5B | $2.1B | $2.1B | -30% | ||

| Mobileye | $458M | $565M | $394M | +16% | ||

| Intel Foundry Services | $118M | $319M | $156M | -24% | ||

As a result, Q1’2023 is a record losing quarter for Intel, with the company posting its biggest loss ever recorded. Even amidst the company’s many ups and downs over the last 54 years, the company has never lost more than a billion dollars in a quarter, let alone over two billion. Admittedly, part of this is structural – restructuring charges, share-based compensation costs, income taxes, and other non-core elements contributed over $2 billion in GAAP net losses – but the size is still staggering.

Consequently, Intel’s highly vaunted gross margin dropped to just 34.2%, its lowest in at least 20 years.

And yet, despite all of this, this quarter went better than expected for Intel. The company had warned investors early-on that it would be brutal, and while Intel delivered on those promises, it exceeded its revenue and EPS projections from earlier in the quarter. So while the company is far from being out of its current slump, there are some signs that it may be nearing the bottom.

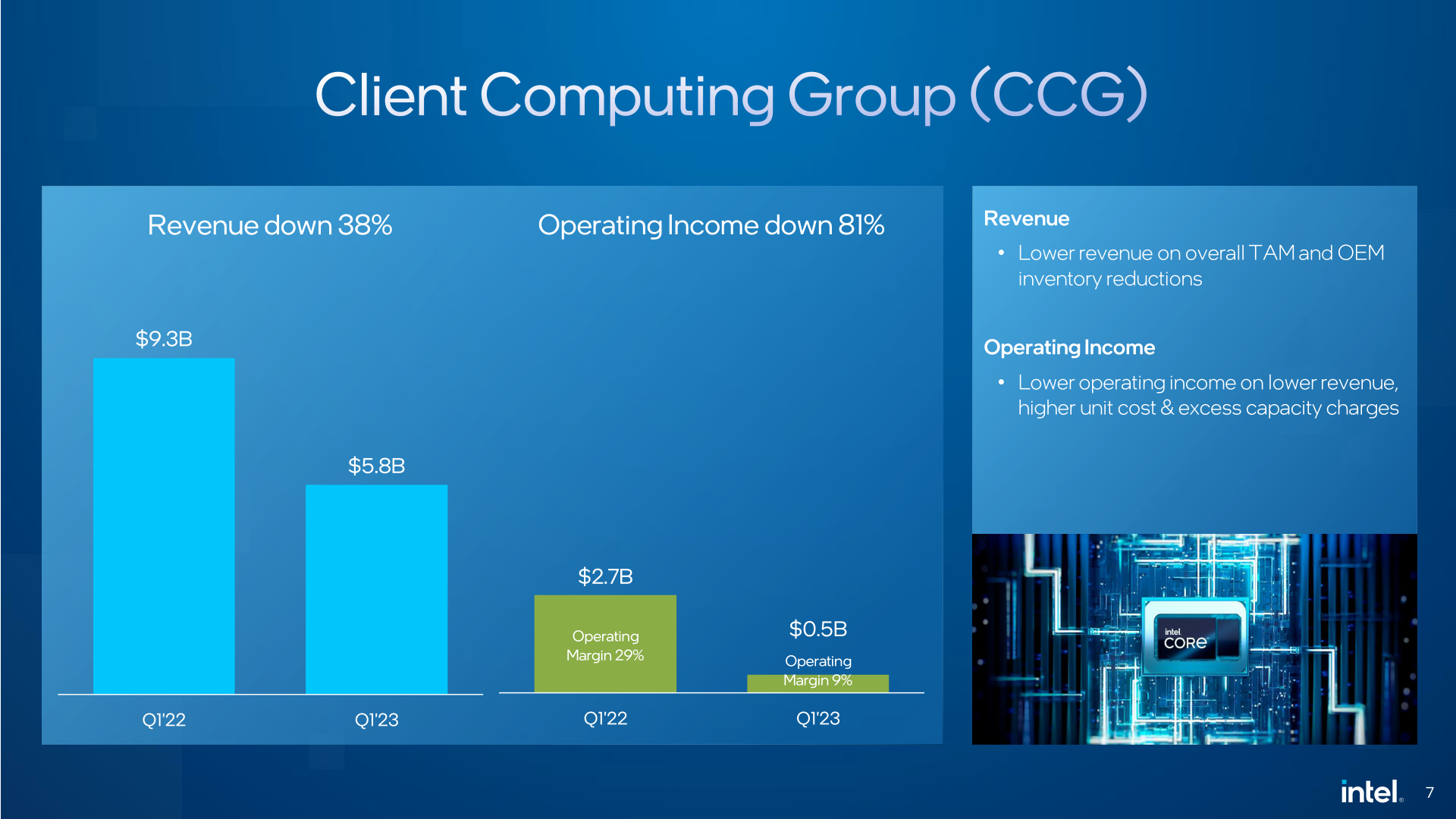

Diving into individual segment performance, the Client Computing Group (CCG) remains the bellwether for the company. Unfortunately, its also one of the segments being hit hardest by the tech spending downturn, with tech companies across the globe recalling from a 30%+ drop in PC sales.

To that end, Intel booked $5.8B in client revenue for the quarter, which is down 38% from the year-ago quarter. Despite all of this, the CCG maintained a positive operating margin, coming out ahead by $0.5B, for a 9% margin. Looking at Intel’s detailed report, laptop sales dropped harder than desktop sales, though both were down significantly. At this point Intel’s downstream OEM customers are still burning through previously purchased inventory, which means that Intel is selling far fewer chips than is usual. Intel stopped providing ASP information some time ago, so it’s unclear how much a change in chip pricing is also a factor.

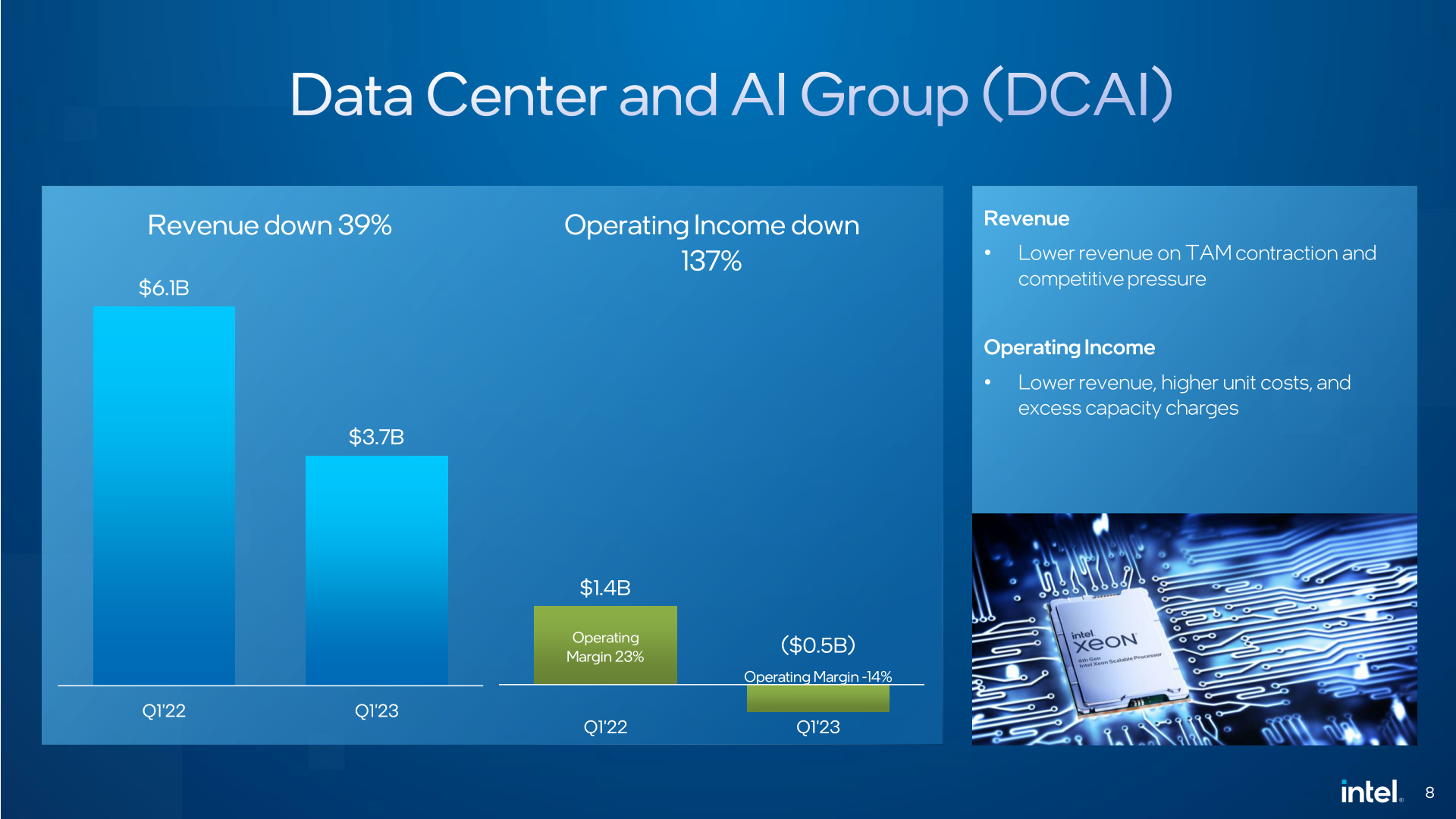

Moving on, Intel’s Data Center and AI Group (DCAI) is recovering from problems of its own. While Intel is now shipping its long-overdue Sapphire Rapids processors in volume, they are still ramping up in order to hit their goal of 1 million chips sold by mid-year. In the interim, DCAI sales have softened even more than client sales, with revenue dropping 39% from the year-ago quarter, despite Sapphire Rapids finally being out the door.

For the quarter, Intel booked just $3.7 billion in DCAI revenue. Which on an operational basis translates to a $518M loss for the company. The fact that Intel took a loss on its data center segment is remarkable, although not for good reasons. While the data center/server business has been reconfigured multiple times over the last decade, I cannot recall it ever operating at a loss – and checking around, this seems to be correct. Despite being what’s traditionally Intel’s highest margin business unit, Intel was unable to eek out even an operational profit on server parts for the quarter.

Complicating matters somewhat has been yet another organizational change within Intel. The Accelerated Computing and Graphics Group (AXG), which was previously a top-line business unit, was split up and subsumed late in December by the CCG and DCAI business units, with each taking their respective half of the business. The modern incarnation of AXG is now solely focused on datacenter parts, and is a part of DCAI. I bring this up because as a fledgling business unit, AXG itself was running an operating loss in 2022. Per Intel’s revised figures to allow for like-for-like, year-over-year comparisons with their revised business units, the combined business unit shift knocked nearly $300M off of DCAI’s operating income for Q1’2022. There’s no way to tell what the impact was for 2023, but it seems unlikely that AXG was positively contributing to DCAI’s profitability.

The final of Intel’s big groups is the Network and Edge Group (NEX), which covers Intel’s networking, connectivity, and IoT products, and is where Intel records sales of other silicon such as Xeon SKUs for networking products. NEX has taken a similar hit as Intel’s other top-line groups, with revenues falling 30% to $1.5B. This was enough of a drop to also push NEX into the red, losing $300M for the quarter. According to comments from Intel CEO Pat Gelsinger, the NEX customer base is enacting similar inventory corrections as some of the other chip units, which will continue for a couple more quarters.

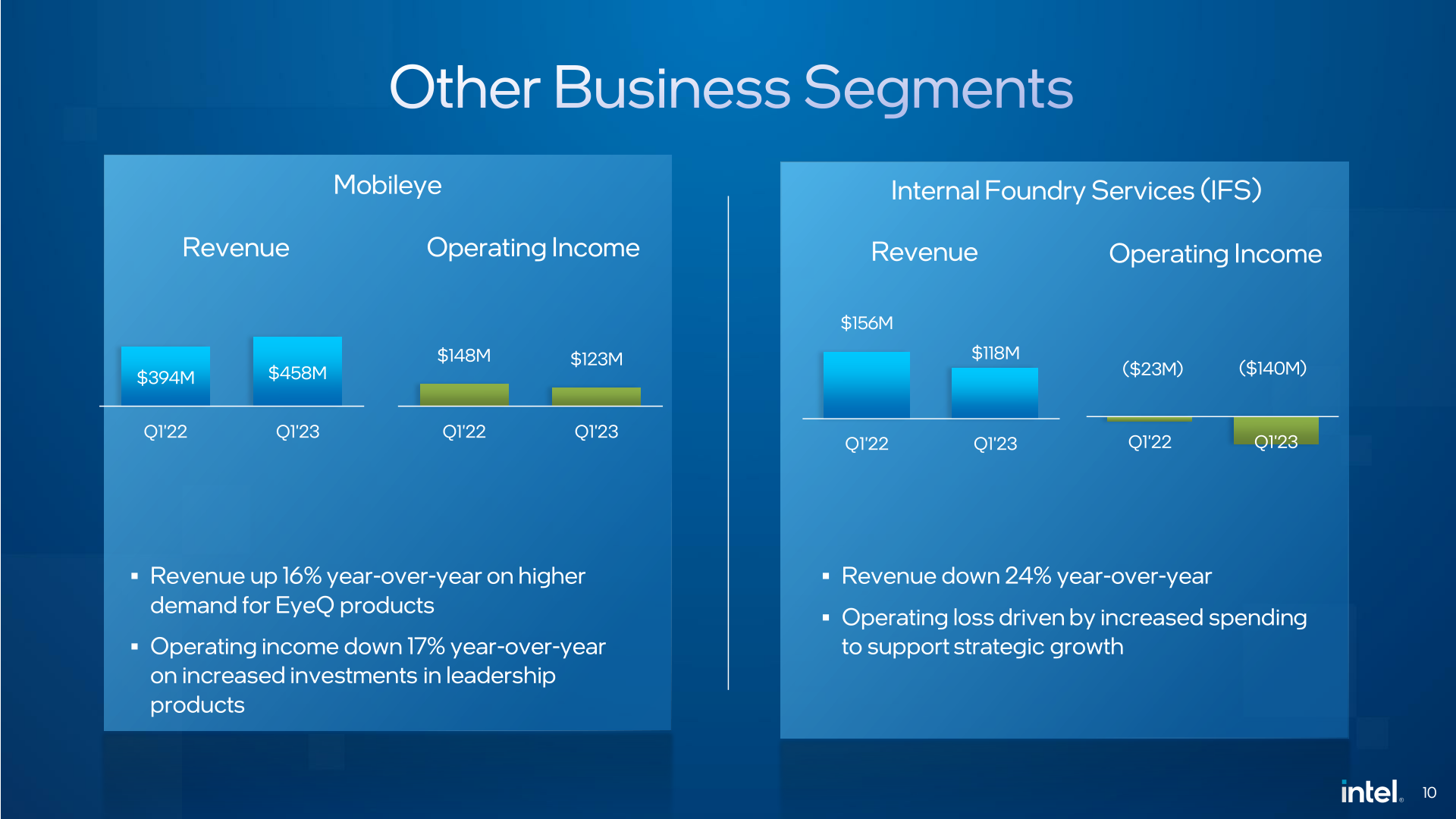

Rounding out Intel’s portfolio, Mobileye was the one distinct bright spot in Intel’s earnings report. The automotive group has seen revenue grow year-over-year by 16%, reaching new records for the quarter. And while operating incomes were down by 17%, it’s still operating in the black. Intel Foundry Services (IFS) on the other hand was in the red, though this isn’t unexpected as Intel is still in the midst of a multi-year investment strategy to retake fab performance leadership. Revenue dropped 24% year-over-year, but Intel has made it clear that IFS is a long-haul prospect that they will continue to invest heavily in.

Looking forward, while Intel is indicating that parts of its business segments have bottomed out (or nearly so), Q1 was not the last bad quarter for Intel. For Q2’2023 the company is projecting revenues of $11.5B to $12.5B, which would be a 22% YoY drop. Gross margins are expected to drop further as well, to a GAAP gross margin of just 33.2%. As noted earlier, the company is projecting a modest recovery in the second half of the year, but they will still have to get through Q2 to get there.

Following Q1, Intel’s major overall initiatives remain unchanged, both with regards to product plans and operational expenses. As announced last year, the company is undertaking efforts to significantly cut expenses; and according to Pat Gelsinger, Intel is “well on our way” towards reducing costs by $3B in 2023, reaching an annual savings of $8B to $10B by the end of 2025.

Otherwise, Intel does not have any major product launches on its public roadmap for Q2 to significantly change the status quo. However, one bright spot in terms of hardware development is that Intel’s next-generation Intel 4 production process and associated Meteor Lake client CPU have entered production, with further ramping taking place throughout the year. As Intel needs to deliver on five nodes in four years to have a serious chance at retaking leadership in the fab market, this is a promising sign that they are indeed on track.

Source: Intel

9 Comments

View All Comments

JayNor - Friday, April 28, 2023 - link

PSG reported revenues up 36% YOY.Intel reported fast ramp to 1 million SPR within 1H.

Meteor Lake ramping for 2H launch.

Emerald Rapids on track for 2H launch.

Gaudi 2 is getting good press from Hugging Face.

Intel 18-A taped out for Lunar Lake first silicon.

Sierra Forest and Granite Rapids, both on Intel 3, are sampling in high volumes.

Qasar - Friday, April 28, 2023 - link

" Intel reported fast ramp to 1 million SPR within 1H.Meteor Lake ramping for 2H launch.

Emerald Rapids on track for 2H launch.

Gaudi 2 is getting good press from Hugging Face.

Intel 18-A taped out for Lunar Lake first silicon.

Sierra Forest and Granite Rapids, both on Intel 3, are sampling in high volumes. "

unless these products are released, who cares if they are ramping up. it doesnt mean squat if you cant buy them. intel is mostly talk and no action now

ikjadoon - Friday, April 28, 2023 - link

Datacenter is a *loss*? Never in 50 year would I imagine Intel's datacenter unit LOSING money.I mean, if graphics were the key contributor, Intel would've mentioned that, no? Or, is that also a little ... embarrassing to admit?

AMD, Ampere, Arm, etc. must be doing work. I'll be curious what AMD reports on Genoa sales.

ikjadoon - Friday, April 28, 2023 - link

Found the transcript. Intel says AXG's now-combined numbers hurt DCAI margins, but curiously they don't mention AXG's impact on income. This must be a watershed moment at Intel. I don't know why they wouldn't clarify more: people would like to know.>[DCAI's] Operating loss was $518 million, impacted sequentially by lower revenue, higher product costs and investment in leadership products on new process nodes. DCAI margins were also diluted by the merge of the AXG business and inventory reserves tied to the exit of our Server System business.

flgt - Friday, April 28, 2023 - link

Well they didn't really have a competitive product last year. The server parts were getting really old and they must have been almost giving them away to clear inventory. Plus they needed a massive engineering push to get SPR out the door. Not good conditions for being able to run a profitable business. The losses would have happened sooner if the chip shortage had not distorted the market so much.Threska - Saturday, April 29, 2023 - link

Well I imagine in some third-world country "almost giving them away" would be music to someone's ears.ikjadoon - Saturday, April 29, 2023 - link

>Well they didn't really have a competitive product last year.These are Q1 2023 datacenter revenue & income. SPR shipments have been ongoing for ~2.5 months, and it's been delayed for years—I would've assumed customers were ready on Day 1 of Q1 2023 to accept product (as validation & ramp finished in Nov 2022 with some orders delivered already)

Though you might be right: perhaps the datacenter division is still recouping costs SPR re-spin.

Some think Intel's 10-Q filings shows a large $2b inventory loss on "non-qualified products"— I can't seem to tease it out as they also lump inventory there…but why would Intel write off $2b in inventory unless it was literally dead?

Shame, shame, shame. SPR started in 2018…you'd think Intel would've learned its lessons in slowing down and not biting off more than it can chew.

Oxford Guy - Saturday, April 29, 2023 - link

‘with tech companies across the globe recalling from a 30%+ drop in PC sales.’Recoiling

zamroni - Sunday, April 30, 2023 - link

Intel past money bosses thought buying euv machines wasn't needed